By Fortitude Investment Partners

Australia’s wave of retiring founders in industrial businesses deserve high quality transitions to future ownership.

Fortitude sees a material opportunity to create value for rolling founders and their teams through empathy for the history of business, and clarity of the opportunity for the future. Fortitude has recent and relevant experience in partnering with industrial distribution businesses and we believe that we have the right combination of empathy and clarity to be great partners.

OVERVIEW

Long dismissed as low-growth and low-multiple, these industrial platforms which have often been in operation for multi-decades can reach their full potential by adding experienced executives to enhance customer intimacy through horizontal integration, combining core distribution or services with adjacent consumables, maintenance and compliance-led offerings. This shift, combined with the use of analytics for resource allocation, transforms transactional revenue into recurring income, lifts margins, improves cash conversion and materially enhances quality of earnings.

Drawing on Australian market dynamics and global case studies, this paper shows how Fortitude deploys disciplined horizontal integration to turn overlooked industrial businesses into scalable, high-quality platforms, rewarding founders who retain stakes alongside Fortitude in the evolution.

INTRODUCTION

Much has been written about the impending baby boomer exit ‘silver tsunami’, where a large number of majority shareholders in small to medium Australian businesses are approaching retirement. The Australian Small Business and Family Enterprise Ombudsman indicates 22% of small businesses in Australia are owned by individuals older than 601. The ABS reports that approximately 68,000 of these entities employ between 5-19 employees.2

We at Fortitude believe a large number of these are high quality, traditional, industrial exposed businesses, which have strong foundations for expansion with the addition of management capabilities. These include companies entrenched in logistics, maintenance, and supply of physical goods to institutional and commercial clients. Examples include industrial distribution businesses to infrastructure, niche areas such as industrial laundry products, safety equipment, testing, inspection, calibration and certification businesses across a wide range of verticals, and industrial ‘soft’ services such as cleaning and security.

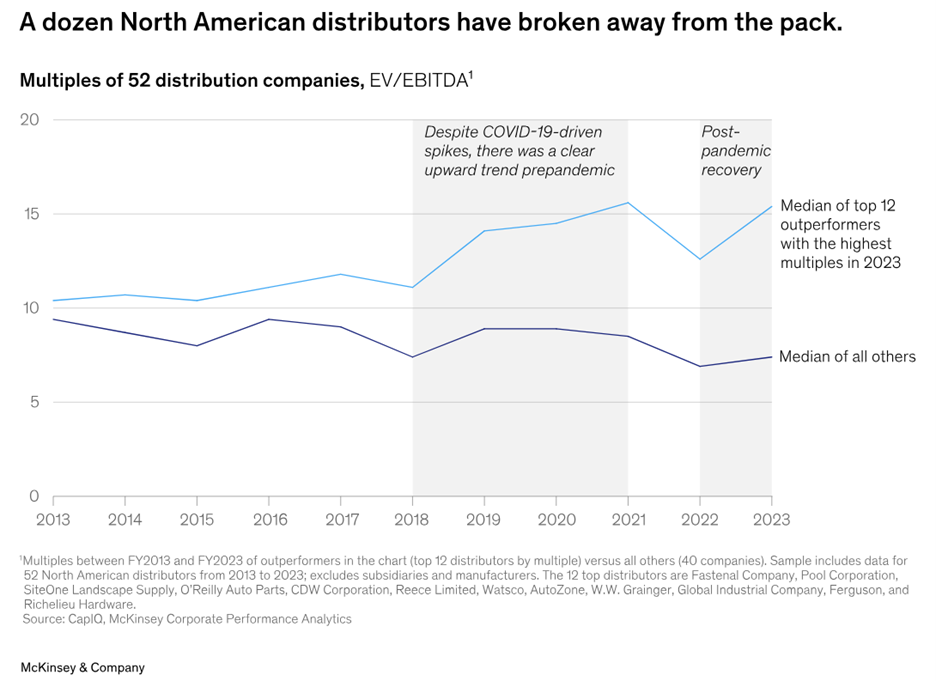

Research from McKinsey & Company shows the significant difference between average quality industrial distribution businesses and those with superior traits as significant and worthy of the evolution to superior. At the time of research, the top 12 outperformers had a median multiple of >15.0x EV / EBITDA as compared to the median of all others being <8.0x.

Valuation Premium of Outperformers

1. Market Context: Why do we like these “Industrial Platforms”?

Structural Attractiveness of Industrial Platforms

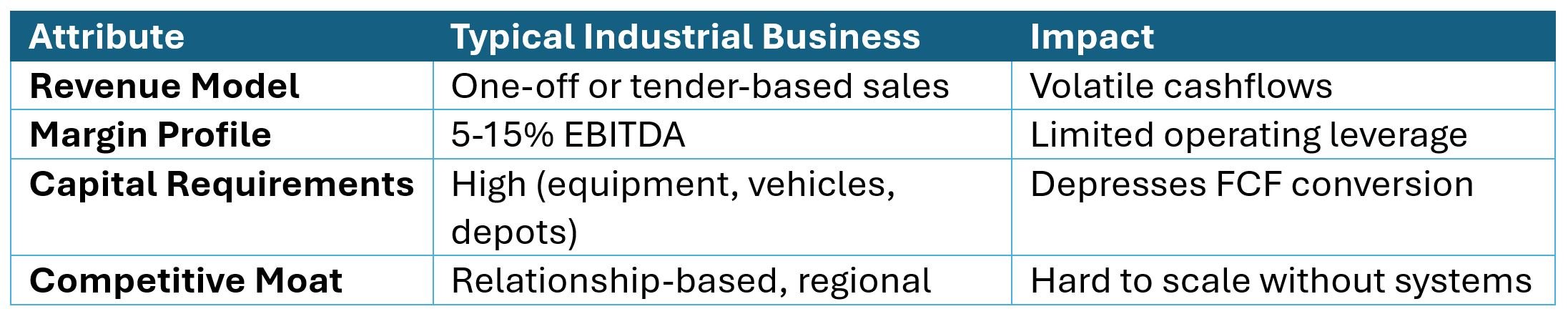

Australia is home to a large number of businesses which have a long history, strong customer-oriented culture, are often real-asset backed and highly cash flow generative.

These companies benefit from:

Less-discretionary demand we particularly like businesses that distribute specialty products to customers in healthcare, defence, aged care, food, and infrastructure services sectors. Our preference is for niche and specialised products, preferably distributed through situations where the business doesn’t just “move boxes”, but rather provides true solutions to their customers.

High replacement frequency of consumables and maintenance cycles.

Localised service delivery and competitive barriers, creating barriers to entry for offshore competitors who may not typically have the breadth of coverage of Australian businesses given the relatively small size of the Australian market.

Typical Characteristics

2. Horizontal Integration – Why Add Consumables and Services?

Revenue Recurrence and Predictability

Consumables – such as chemicals, spare parts, safety items, and similar, being added to the revenue mix can transform a ‘transaction’ business into a partially re-occurring revenue model. For instance, a commercial laundry equipment provider that also supplies detergents, uniforms, and hygiene consumables can triple customer touchpoints and smooth revenue volatility.

Services – for example, several businesses distribute industrial weighing and testing products. The addition of ongoing calibration and servicing can materially increase stickiness and quality of earnings for these customers, increasing the likelihood that those customers return to purchase replacement machines at the end of life of current machines.

Margin Enhancement

Higher Gross Margins: Consumables typically deliver 30–40% margins versus 10–20% for core services.

Bundled Value: Customers pay premiums for one-stop solutions combining product, service, and compliance.

Route Density: Salespeople travelling to sites or delivering to sites can benefit from less frequent deliveries and engagements to maximise margin and enable sharper prices in quoting.

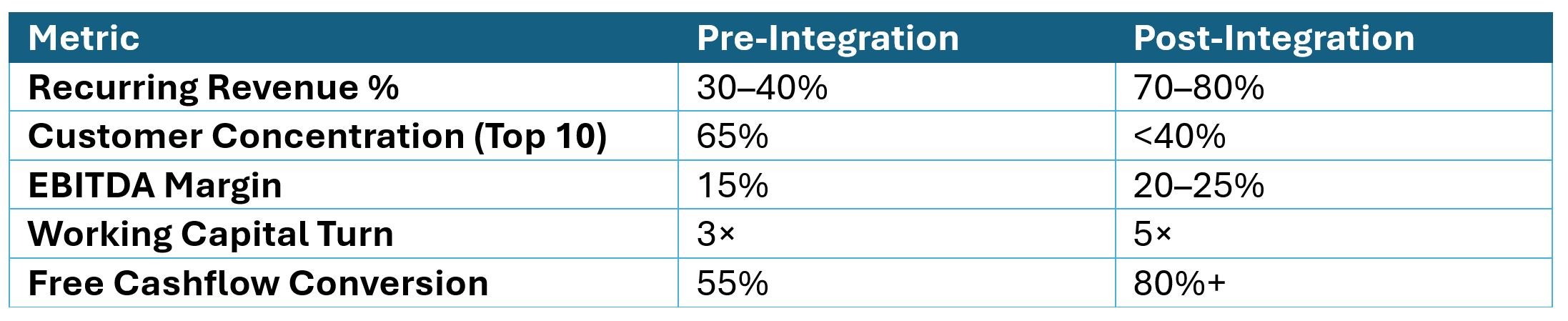

3. Quality of Earnings (QoE) Uplift

Valuation multiples can often be increased with increases in earnings sustainability. That is, the proportion of EBITDA generated from recurring, non-cyclical, contract-backed sources.

Adding consumables and services materially changes the QoE profile. We have included below an illustrative example of how consumables being included into a product or service suite can enhance the QoE.

Quality of Earnings (QoE) Enhancement

Whereas industrial distribution peers might trade in the wide range of 5-8× EBITDA, businesses with stable, recurring consumables income often attract 8–11× at scale.3

4. International case studies

Case Study #1- A&M Capital and Brady Industries

In 2019, A&M Capital (a US mid-market PE firm) invested in Brady Industries⁴. Brady Industries is a US distributor of janitorial & sanitation products (jan-san) with a meaningful laundry products line (chemicals, laundry equipment, warewash, etc.).

Under PE partnership, Brady pursued a classic “adjacent consumables” expansion:

Brady acquired Datek, a distributor of cleaning equipment and janitorial supplies.

It also acquired Maintenance Mart, a regional distributor of janitorial supplies and equipment.

It then bought MASSCO, a distributor of janitorial, office and packaging supplies (i.e., deepening consumables beyond core jan-san).⁵

Brady’s offer increasingly spanned laundry chemicals & equipment, janitorial supplies, foodservice & packaging / facility consumables.

In parallel, Kelso & Company, another US PE firm, owned Individual FoodService (IFS), a distributor of foodservice disposables and jan-san products.

Brady (A&M Capital–backed) and IFS (Kelso-backed) were combined to form BradyIFS, creating a scale platform in: foodservice disposables (consumables), janitorial & sanitation supplies, plus laundry and warewash products as part of the mix.⁶

By 2022, BradyIFS reported >$1.3 billion in annual revenue, with a broad mix of jan-san, foodservice and related consumables.

In 2023, the business was acquired by a Warburg Pincus backed platform for A$2.6bn. We understand the valuation allocated in this merger was compelling, driving a strong return for the shareholder group.

Case Study #2 - CD&R & WESCO Distribution (electrical / industrial products distributor)

1. Initial deal – industrial products distributor

Target: WESCO, the electrical products distribution unit of Westinghouse Electric

Investor: Clayton, Dubilier & Rice (CD&R), a US private equity firm

Year acquired: 1994

Purchase price: ~US$330m⁷

At that point WESCO was a large industrial/electrical distributor selling:

Electrical and industrial products

Communications and utility products

Maintenance, repair and operations (MRO) and OEM supplies

2. Value-creation play – add services & expand consumables / MRO

Operational improvements

Heavy investment in IT and systems

Flattening management layers and enhancing speed of decision-making

Broader consumables / MRO offering via acquisitions

Over CD&R’s hold, WESCO acquired more than US$500m of annualised sales through bolt-on deals.⁸

WESCO’s model evolved into a full-line electrical + MRO + safety consumables distributor with integrated supply chain services.⁹

3. Exit – significantly higher value

Hold period: a little over 4 years

Outcome:

Sales doubled and profits “surged” over the period

In 1998 CD&R sold WESCO to The Cypress Group for around six times its initial equity investment

WESCO was later IPO’d; by 2005 it had US$4.4bn in sales

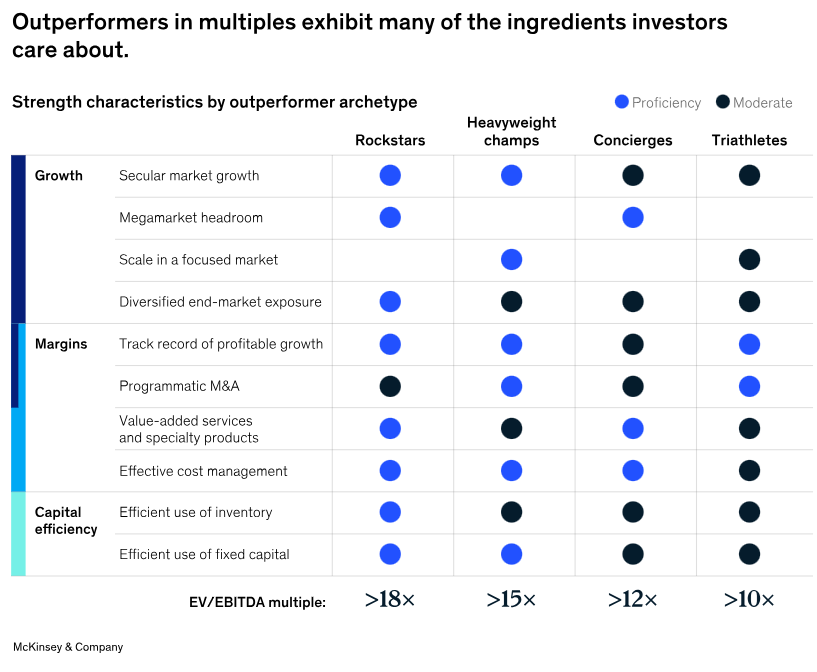

Note that both of the above examples shared traits with the outperformance traits evident in the McKinsey study referred to above.

Outperformance traits and Multiples

5. Implementation – What might this look like in practice?

Step 1: Consider true capabilities of the executive team – can they 3x the business?

Fortitude has over 12 years of experience in recruiting executives to enhance clarity of leadership and performance in SME’s.

We believe our key differentiator is in our ability to match the right style of individual with the organisation’s needs and strategy, considering empathy and culture.

Step 2: Add-On Strategy

Acquire adjacent consumables distributors or service providers with overlapping customer bases.

Prioritise products with regulatory or compliance demand (PPE, hygiene, fire safety consumables).

Step 3: Integration

Truly implement ERP and CRM systems linking customer usage data to consumables ordering and ensure the team is engaged in using this information.

Cross-train sales teams for bundled offerings.

Centralise procurement for volume rebates and supplier leverage.

Step 4: Data & Analytics

Use consumption and route data to predict demand and automate re-ordering.

Track contract renewal rates, delivery density, and gross profit per route as core KPIs.

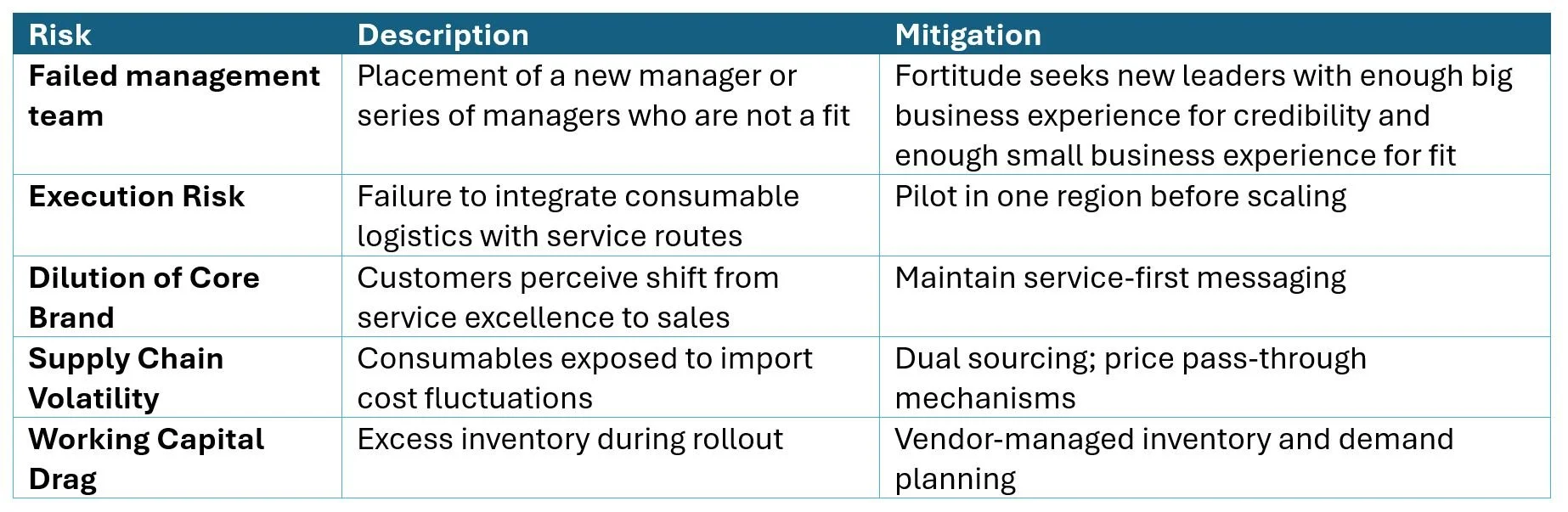

6. Where these strategies fail and possible mitigations

Principal Execution Risks

7. Conclusion: The Next Decade of Industrial Value Creation

In a capital-constrained environment, we think industrial distribution with consumables integration represents one of the most attractive risk-adjusted opportunities for Australian private equity. These businesses combine defensible local operations, contractual customer relationships, and scalable adjacencies.

Adding consumable distribution and associated services converts a “low-multiple, high-asset” model into a resilient, data-rich, and premium-valued platform. The key to success lies in disciplined execution—understanding the route economics, customer behaviour, and integration sequence.

As Australian investors seek durable earnings and inflation-hedged assets, this strategy offers both stability and upside—turning “old-world” industrials into tomorrow’s compounding platforms.

Fortitude is working on four investment opportunities which fit the above narrative (one in industrial laundry products and two in testing, inspection, certification and compliance) and we are happy to discuss the relevance of our experience with Hospital Pharmacy Services, Quality Foods & Beverages, Birch & Waite, Nutra Organics, TEN Group, Machines 4U and other B2B businesses where we have deployed the above strategies.

REFERENCES

[1] Australian Small Business and Family Enterprise Ombudsman

[2] Finder - Business Statistics Australia

[3] Note: These are as evidenced over anecdotal feedback from M&A advisers in Australia.

[4] Alvarez & Marsal Capital Partners

[5] Alvarez & Marsal Capital Partners

[6] MDM Distribution Intelligence - Individual FoodService Merges with Brady Industries

[7] MDM Distribution Intelligence - Private Equity Case Studies

[8] MDM Distribution Intelligence - Private Equity Case Studies

[9] WESCO